AM I OBLIGED TO RETAIN IRPF IN MY INVOICES?

First of all, only certain freelancers are required to retain IRPF in their sales invoices. Companies do not have this obligation, and only need to apply VAT in their invoices, unless we are talking about a rental invoice to another company. In this last case, VAT is added to the taxable base of the invoice and IRPF is deducted from the same taxable base.

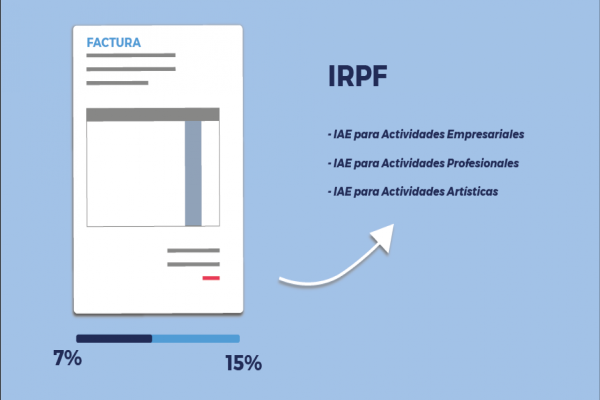

If you are a freelancer, you need to know in what code (epígrafe) of economic activity (IAE) you have been registered. In Spain, freelance activities are divided into business (Sección 1), professional (Sección 2) and artistic categories (Sección 3). Only freelancers that carry out professional activities (doctors, lawyers, teachers, translators etc.) must issue their invoices with income tax retention and only if their clients are other freelancers or businesses in Spain.

If 70% or more of their total income is subject to this retention, they will not have to present the quarterly income tax declaration (Modelo 130). If the clients are private individuals, for example, patients of a doctor or students of a teacher, you do not have to retain IRPF but you do have to present the quarterly income tax declaration.

HOW MUCH TO RETAIN?

At the beginning of a freelance professional activity, you have the possibility of applying a reduced retention in your sales invoices. In this article we clarify the conditions for doing so and its advantages and disadvantages.

Income tax retentions are amounts advanced to the Tax Office on account of the expected result in the income tax return or IRPF. These retentions are deducted in sales invoices to other businesses and the receiver of the invoice (the customer) is obliged to declare and pay the retained amounts.

The personal income tax law establishes a 15% retention for professional activities, but new freelance professionals can retain a reduced rate of 7% for the year of registration and during the following two years. In other words, you can apply this reduced rate to the first three years of your professional activity.

REQUIREMENTS

You can apply the reduced retention if you have not exercised any professional activity in the previous twelve months and if you have communicated to your clients that you are applying 7% retention for starting a professional activity. Your clients are obliged to keep this communication in case of tax inspections.

The communication must include your identification, the date of entry into the activity to justify that you are indeed a new freelance professional and the time you will apply the reduced retention (you do not have to do this for all the years allowed by law). Here is an example of a communication to customers:

REQUEST FOR APPLICATION OF THE REDUCED RATE FOR RETENTIONS IN THE FIRST YEARS OF REGULATED PROFESSIONAL ACTIVITY: Art. 95 R.D. 439/2007

D./Dª................................................................................ , of legal age, DNI...................in..............................street.......................................states:

That in accordance with the provisions of Article 95 of Royal Decree 439/2007, which states

"... in the case of taxpayers who begin to exercise professional activities, the rate of retention will be 7 percent in the tax period in which the activities begin and in the following two, if they have not exercised any professional activity in the year prior to the date of commencement of the activities. For the application of the retention rate provided for in the previous paragraph, the taxpayers must notify the payer of the income of the occurrence of this circumstance, the payer being obliged to keep the communication duly signed ".

I communicate that I registered my professional activity last XX/XX/XXXX and by means of this letter the application of the reduced 7% retention on my professional income for the years XXXX, XXXX and XXXX.

It is important that you communicate this to all your clients who are obliged to retain. Even if you issue your invoice with 7% IRPF, your clients will have to retain 15% on account of IRPF if they do not receive this communication.

Similarly, if you receive invoices from other professionals in which they apply the reduced 7% retention, you must ask them for the communication, duly signed. Keeping this documentation is important as it is the person who receives the invoice who is obliged to apply the retention correctly and pay the accumulated retentions to the Tax Office every quarter.

TO RETAIN OR NOT TO RETAIN?

Applying a reduced retention is not obligatory, and you must evaluate if it is of your interest. If the deductions made during the year have been too high, when the time comes to present the IRPF return, it will be returned. If the withholdings have been low, you will have to pay.

Advantages: Applying the 7% retention allows you to have more liquidity, something positive at the beginning of the activity if you do not have too much income.

Disadvantages: If your business takes off strongly and you make a profit from the first moment, you will have to pay more when filing your income tax return because you have advanced less than if you had applied the general 15% retention.

If your client is not established in Spain but in the EU or other parts of the world, no retention on your sales invoices is required.

First of all, only certain freelancers are required to retain IRPF in their sales invoices. Companies do not have this obligation, and only need to apply VAT in their invoices, unless we are talking about a rental invoice to another company. In this last case, VAT is added to the taxable base of the invoice and IRPF is deducted from the same taxable base.

If you are a freelancer, you need to know in what code (epígrafe) of economic activity (IAE) you have been registered. In Spain, freelance activities are divided into business (Sección 1), professional (Sección 2) and artistic categories (Sección 3). Only freelancers that carry out professional activities (doctors, lawyers, teachers, translators etc.) must issue their invoices with income tax retention and only if their clients are other freelancers or businesses in Spain.

If 70% or more of their total income is subject to this retention, they will not have to present the quarterly income tax declaration (Modelo 130). If the clients are private individuals, for example, patients of a doctor or students of a teacher, you do not have to retain IRPF but you do have to present the quarterly income tax declaration.

HOW MUCH TO RETAIN?

At the beginning of a freelance professional activity, you have the possibility of applying a reduced retention in your sales invoices. In this article we clarify the conditions for doing so and its advantages and disadvantages.

Income tax retentions are amounts advanced to the Tax Office on account of the expected result in the income tax return or IRPF. These retentions are deducted in sales invoices to other businesses and the receiver of the invoice (the customer) is obliged to declare and pay the retained amounts.

The personal income tax law establishes a 15% retention for professional activities, but new freelance professionals can retain a reduced rate of 7% for the year of registration and during the following two years. In other words, you can apply this reduced rate to the first three years of your professional activity.

REQUIREMENTS

You can apply the reduced retention if you have not exercised any professional activity in the previous twelve months and if you have communicated to your clients that you are applying 7% retention for starting a professional activity. Your clients are obliged to keep this communication in case of tax inspections.

The communication must include your identification, the date of entry into the activity to justify that you are indeed a new freelance professional and the time you will apply the reduced retention (you do not have to do this for all the years allowed by law). Here is an example of a communication to customers:

REQUEST FOR APPLICATION OF THE REDUCED RATE FOR RETENTIONS IN THE FIRST YEARS OF REGULATED PROFESSIONAL ACTIVITY: Art. 95 R.D. 439/2007

D./Dª................................................................................ , of legal age, DNI...................in..............................street.......................................states:

That in accordance with the provisions of Article 95 of Royal Decree 439/2007, which states

"... in the case of taxpayers who begin to exercise professional activities, the rate of retention will be 7 percent in the tax period in which the activities begin and in the following two, if they have not exercised any professional activity in the year prior to the date of commencement of the activities. For the application of the retention rate provided for in the previous paragraph, the taxpayers must notify the payer of the income of the occurrence of this circumstance, the payer being obliged to keep the communication duly signed ".

I communicate that I registered my professional activity last XX/XX/XXXX and by means of this letter the application of the reduced 7% retention on my professional income for the years XXXX, XXXX and XXXX.

It is important that you communicate this to all your clients who are obliged to retain. Even if you issue your invoice with 7% IRPF, your clients will have to retain 15% on account of IRPF if they do not receive this communication.

Similarly, if you receive invoices from other professionals in which they apply the reduced 7% retention, you must ask them for the communication, duly signed. Keeping this documentation is important as it is the person who receives the invoice who is obliged to apply the retention correctly and pay the accumulated retentions to the Tax Office every quarter.

TO RETAIN OR NOT TO RETAIN?

Applying a reduced retention is not obligatory, and you must evaluate if it is of your interest. If the deductions made during the year have been too high, when the time comes to present the IRPF return, it will be returned. If the withholdings have been low, you will have to pay.

Advantages: Applying the 7% retention allows you to have more liquidity, something positive at the beginning of the activity if you do not have too much income.

Disadvantages: If your business takes off strongly and you make a profit from the first moment, you will have to pay more when filing your income tax return because you have advanced less than if you had applied the general 15% retention.

If your client is not established in Spain but in the EU or other parts of the world, no retention on your sales invoices is required.